For more than three decades, the Scottsdale Institute has been a quiet pivot point for the industry's most senior healthcare technology figures — an invite-only enclave where CIOs and technology veterans gather far from the marketing clamor of typical trade shows. The atmosphere is scholarship, not salesmanship. It's the kind of room where Judy Faulkner, the founder of Epic Systems, can be found settled in a chair with her attention fixed on a yellow legal pad, scribbling notes for hours. Where Micki Tripathi, the former head of ONC, sits and chats with whoever walks by. The discourse is granular. People skip the high-level platitudes and go straight to the specific, nuanced mechanics of how complex health systems are actually built and sustained. It's a place where the quiet part can be said out loud.

By the second day of the four-day marathon — sunrise to dinner, repeat — the professional veneer you'd find in a typical boardroom starts to soften. Faces become familiar over shared coffee and cocktails. The tenor of the room shifts toward a rare openness. In an industry usually guarded by proprietary secrets, this summit has become a sanctuary for curiosity and the kind of peer-to-peer intelligence sharing that senior executives say is increasingly hard to find anywhere else.

I left Scottsdale with one belief sharpened: AI governance in healthcare is quietly transforming from a risk-management function into something much closer to portfolio management. The systems that figure this out first will be the ones that survive what's coming. What follows is what I heard, what's actually working in the field, and where I think the discipline is headed.

Healthcare is being defunded, and health systems are going to get hit hard. You could feel the lament in the room — leaders absorbing meaningful federal funding compression while still trying to operate on the razor-thin margins that have defined the sector for years. This isn't hyperbole: about four in ten hospitals had negative operating margins in 2023, and indexed adjusted operating margin sat at just 1.3% at the end of 2025. More than 300 rural hospitals are currently at "immediate risk" of closure.

And the pain hasn't even fully landed yet. The 2025 reconciliation bill (OBBBA) includes roughly $1 trillion in projected Medicaid cuts, with three-quarters of those cuts hitting in the last five years of its 10-year implementation. 66% of healthcare finance leaders cite government funding and Medicaid cuts as their leading concern — no other issue (labor costs, payer negotiations, margin compression) was named by a majority.

Many systems are closer to bankruptcy than the public realizes. But there was also a willingness to step up. As one leader put it: "We've always dealt with hard problems in healthcare. This isn't new."

There is a strong, general sentiment that AI — while recognized as just a new technology — may be the best available lever for the billions in revenue health systems are about to lose to regulatory contraction.

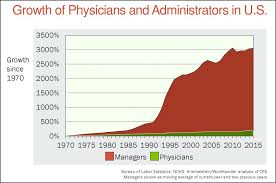

Healthcare has adopted AI faster than any other industry, partly because of the overwhelming amount of cost stuck in administrative overhead. Since the 1970s, the industry has more or less plateaued in producing providers, while the number of healthcare administrators grew roughly 3,200% between 1975 and 2010, compared to 150% growth in practicing physicians. There are now, by some estimates, 10 administrators for every physician in the United States. That's the cost basin AI is being aimed at.

I had a chance to sit down with leaders from a few of the largest health systems in the US — the big ones — and got a detailed look at where they were investing in AI, where they were seeing strong ROI, and importantly: how they were picking, testing, deploying, and tracking ROI across all these initiatives.

Five major, thematic buckets of use cases kept surfacing — areas where both hard and soft ROI were clear enough to scale in big ways.

This is the longtime workhorse, and investment keeps compounding. ROI is clear, and the most effective evaluation method is retrospective: a simple question — how many cases would we miss if we fed this thing a bunch of old data? The tricky part: this has to be conducted in a legally safe place. Finding missed cases is no bueno because it represents potential malpractice. But all good things have an ethical solution; in this case, conducting these studies within enclaved patient safety groups. Prospective ROI is relatively straightforward — tie baseline metrics to new cases, codes, and procedures. The procedure codes and reimbursement mechanics, however, can be fraught.

The meteoric rise of ambient scribes has been an absolute success story — but for all the reasons we didn't originally build our hypotheses against. Originally pitched as a mega-time-saver for clinicians, that argument has slowly (and now rapidly) eroded. A recent JAMA study tracking over 1,800 clinicians across five academic medical centers found modest daily reductions of just 13 minutes in EHR usage and 16 minutes in documentation time — relative decreases of 3% and 10%. After-hours charting didn't change significantly. Doctors using ambient scribes were still doing notes at slightly better rates than doctors who didn't.

Modest numbers. Scaled across thousands of providers, sure, that adds up — but not what we originally thought.

Instead, the value of ambient has shown dramatic soft ROI. Providers friggin' love it. It's reducing pajama time in ways the time-savings data doesn't fully capture, and it's become a tool you can't take away from them. Mass General Brigham observed a 21.2% reduction in burnout prevalence after 84 days of ambient documentation. That's the real story.

Hard ROI is starting to creep in too — through coding. In the lower 15% of coding-accurate provider groups, automated uplift has pushed them into the 85%+ range. That accuracy has clear reimbursement ROI that would otherwise be left on the table. A 2025 UCSF study in JAMA Network Open found that physicians using AI scribes generated an average of $3,044 more revenue per year and saw 0.8 more patients per week compared to non-users.

ROI tracking is harder here than it looks. EMRs don't have great data on "time in chart," so it takes real effort. Provider satisfaction surveys, coding improvements, burnout scores, and visit-volume deltas all need to be triangulated.

Voice and chat are the stars of the show. Call centers have been bottlenecks for years and simply can't keep up with demand. A sentiment kept emerging in the room: AI will of course demonstrate cost reduction via automation and FTE relief — however — the more interesting nuance is that this cost reduction won't likely affect the bottom line until demand is satisfied.

Why? Picture 50 FTEs doing patient outreach against a list of 10,000 patients who need a call. You can add AI to automate outbound calling at huge volumes and never crawl out of that demand pit. Your costs will only go up as you spend more on AI plus your FTEs. Ultimately, AI may be pushing growth and revenue much more than reducing cost.

This is an important nuance to grok as we think about how AI impacts the economics of our healthcare institutions. And it's not just inbound — patients are demonstrating an enormous appetite to interact with healthcare differently. More on that below.

RCM is emerging as an ROI gem in a big way. My hunch is this is where health systems will see the biggest hard ROI numbers. Claims processing, letter drafting, prior auth, contract dispute resolution — all winning the AI ROI battle. The data backs this up: AI prior authorization spending is growing 10x year-over-year — from $10 million in 2024 to $100 million in 2025, and 92% of healthcare leaders cite AI and advanced automation as a top investment priority in 2025, particularly within patient access.

Much to payers' chagrin, I expect a battle to ensue between provider and payer AI solutions going back and forth, fighting over costs and charges. It's already started. UnitedHealth has launched Optum Real, a real-time claims system delivering instant coverage validation, while AI tools on the payer side have been accused of producing care denial rates in some cases 16 times higher than typical. Provider-side AI is now arming up to push back. The arms race is real, and it's where some of the biggest hard-dollar AI value is going to live in the next 24 months.

There's a plethora of narrow, specific use cases — common across every health system but also tailored to the priorities of specific ones. One example that came up multiple times: inpatient lab and medication ordering. Some health systems have 500+ pharmacists on staff to facilitate these transactions. AI takes a first pass — sorting orders into (a) simple and easy and (b) complex and difficult — and ensures the order is correct, formatted, and has a high chance of going through clean and fast.

Health systems are increasingly using agentic tools (Agent Factory and similar platforms) to spin these up. They're tested, run through standardized governance, and POC'd just like any other tool. Each one alone looks small. In aggregate, the portfolio is significant.

There was a lot of conversation about what a POC is — and isn't. Even more about ROI tracking and the discipline required to manage ROI across a portfolio of hundreds of AI tools.

Health systems are running a lot of pilots, and most are framed as experiments rather than ROI proof points. CFOs are applying real pressure on financial impact, but POCs are typically meant to gauge how a tool actually works in real-world settings with real-world users. Reading about how an AI tool processes data is one thing; having a provider field its alerts during a busy ICU shift is another. POCs can extend much longer than vendors expect — and AI vendors need to prepare for that. Flexibility and rapid iteration, probably for several years, is the price of finding the right workflow fit.

Even after a POC, the scrutiny doesn't end. Across many of our customers, I'm watching a kind of post-deployment culling underway. Questions like "Which AI tools are generating positive ROI and which are not?" have moved from rare to common in less than two years.

One quote stayed with me longer than any other from the trip:

"AI moves at the speed of trust for health systems. AI moves at the speed of desperation for patients."

That second half lands harder when you look at the numbers. Of more than 800 million regular ChatGPT users, roughly one in four submits a healthcare-related prompt every week, and more than 40 million people do so daily. An OpenAI survey conducted in December found that three in five U.S. adults had used an AI tool for health or medical questions in the prior three months. About 70% of health-related conversations on ChatGPT occur outside normal clinic hours.

Patients aren't waiting. They're using LLMs to decode medical bills, spot errors, appeal insurance denials, and decide whether to seek urgent care. Nearly one in three Americans said they would delay or avoid seeing a doctor if an AI tool labels their symptoms as low risk. That last one should make every health system leader sit up.

Healthcare must move quickly if it wants to stay relevant. Compounded by the defunding coming, this isn't a new regulatory requirement we need to plan for — it's a life preserver that has to be wielded with highly complex considerations. Patients are sprinting toward AI. Health systems are trying. The gap between those two speeds is where competitive positions will be made or lost over the next few years.

AI governance was, of course, a major theme. Every hospital I spoke with has an AI governance committee, an evolving set of policies and procedures, and is working through different mandate configurations between sub-groups. Committee structures remain tribal and bespoke — federated, centralized, agile, hybrid — and there is real diversity in how organizations split decision rights across them.

A few findings stood out. The mandate of AI committees is expanding well beyond risk management into what I'd call benefit management — taking institutional priorities, comparing solutions that map to those priorities, evaluating tools for both risk and AI-initiative fit, and managing all of it as a portfolio.

This is the observation we've built Onboard AI around: AI governance committees are not just risk gates anymore. They're where the AI portfolio gets shaped. The systems that operationalize this work will compound advantage. The ones that keep treating it as a series of one-off approvals will quietly fall behind.

Forty-eight hours in Scottsdale didn't change my view of where healthcare AI is going. It changed my view of how fast and how disciplined the institutions need to get there — in the face of yet another round of major challenges.

The speed of trust is going to have to pick up. The speed of desperation already has.